Introduction

The proposal you are about to read will significantly lower taxes for the vast majority of individuals and corporations. This is accomplished by making everyone pay their fair share of the tax burden, and when everyone pays their fair share, even though overall taxes are lower, sufficient revenue is still raised to:

- Fully fund public education to include free college or vocational school.

- Expand Medicare into National Health Care.

- Increase Social Security benefits upon retirement.

- Retrain unemployed and displaced workers.

- Repair our deteriorating infrastructure.

- Create millions of high paying jobs.

- Transition our economy to renewable, non-polluting energy.

All this is possible by restructuring the way we raise taxes and re-prioritizing our spending policies. However, before any serious reform can take place we must first identify the main problem that makes our current tax code inadequate, inequitable, and incomprehensible: the tax deduction.

The dictionary defines a tax deduction as an expenditure that is deducted from taxable income. Examples include charitable contributions that can be deducted from one’s taxable income, the interest on home mortgages, opulent buildings that corporations buy or rent, and exploration expenses when searching for natural resources. There are tax breaks for business meals and entertainment, corporate jets, country club memberships, mergers and acquisitions and accelerated depreciation.

More egregious examples include the “check-the-box” loophole, the “Hewlett-Packard” loophole, the “Real Estate Investment Trust” loophole, the “carried interest” loophole, the “earnings stripping” loophole, and the “valuation discount” loophole.1

The list goes on and on, and the mere existence of one deduction is used as the justification to create even more deductions whether they are geared to benefit society as a whole or the narrow interests of the few.

To date, the tax code is over 13,500 pages, and every year it increases because every year politicians create new deductions in response to the desires of some of their influential constituents who want to pay less in taxes. This misuse of our legislative system allows wealthy individuals and corporations to avoid paying their fair share of the tax burden, forcing a disproportionate percentage of the tax obligation onto those who cannot access these deductions – the middle class and the working poor. The result is a decrease in the amount of revenue needed to properly fund the programs and services our society deems important, and leads directly to waste, fraud, and corruption.2

Therefore, the best first step we can take to correct this problem is to eliminate all tax deductions, and that is the signature achievement of this plan. This proposal eliminates all deductions with no exceptions. A tax system absent all deductions allows for simple solutions to the inherent complexities of taxation, and when combined with the reprioritization of our spending policies results in a tax code that is simple and fair and equalizes opportunities for everyone.

No serious attempt at tax reform can occur without addressing the three major programs that account for 62% of our annual budget: Social Security (22%), Medicare, Medicaid and CHIP (21%), and defense (19%).3 This proposal successfully addresses the self-funding problems associated with Social Security and health care, and calls for a special National Security Surtax to be shared by all American taxpayers to cover defense spending that exceeds two time the combined amount that Russia and China spend on their military budgets.

This proposal is not an attempt to solve all tax problems. As stated in the title, it is a “framework,” a guide for tax reform. It addresses major areas of concern, and uses the principles of simplicity and fairness to solve them. Its purpose is to be the basis for the legislation that will be used to enact these reforms into law.

I would like to thank Sisters Theresa LaMetterey, CSJ and Ann Marie Steffen, CSJ for their assistance in the preparation of this document. Their straightforward questions, formatting and editing skills and tireless work made all this possible. I would like to thank my brothers, Jay and Ray Fishman and my sister-in-law Joyce, for their piercing questions, logical criticisms, and suggestions. And, to Julie Muyco, for providing the tax revenue estimates for the original manuscript (published in 2007).

For the revised and updated 2015 edition, I would like to express my gratitude to Ashford Wallace for his time and assistance in not only editing this manuscript, but also for his insightful ideas and advice which were invaluable in helping me complete this book, and to thank Kathryn Bundy for her astute suggestions, patience, and editing skills.

Mark Lewis Fishman

Executive Summary

This proposal will lower taxes for the vast majority of Americans and corporations while still raising sufficient revenue to fully fund and expand the programs and services our society deems most important: Medicare, Social Security, and Public Education. It accomplishes all this and more while running a budget surplus.

A brief synopsis of how this is accomplished is presented below.

1. BusinessTaxes

a. Business Gross Sales Tax

The major problem with the existing tax code is that it penalizes corporations with higher taxes as they become more profitable. This encourages the use of deductions to lower the net profits so that the corresponding tax liability is reduced.

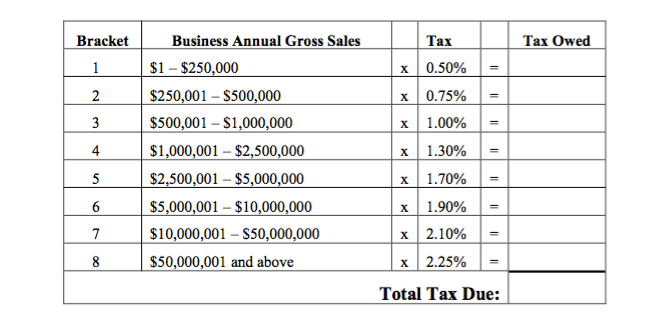

Section 1.a. eliminates the need for deductions by replacing the tax on net profits with a small tax on gross sales. The Business Gross Sales Tax would look like this:

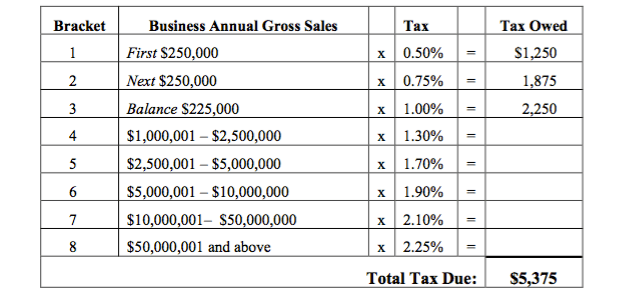

EXAMPLE – To calculate the Business Gross Sales Tax on annual gross sales of $725,000:

- Separate the annual gross sales into the corresponding brackets.

- Multiply by the corresponding tax and place this amount in the Tax Owed column.

- Add up the Tax Owed column to determine the Total Tax Due.

In this example, the Business Gross Sales Tax on a corporation with annual gross sales of $725,000 is only $5,375. Since the tax on gross sales remains the same no matter how high profits might increase to, the tax on gross sales rewards business for being more profitable by not increasing taxes as profits rise. And, since the tax on gross sales makes all corporations pay their fair share, federal business tax revenue will increase from $329.3 billion (fiscal 2012)4 to at least $662.2 billion per year.5 This means that over the next ten years the Business Gross Sales Tax will bring in an additional $3.32 trillion to the treasury.

b. Business Payroll Taxes

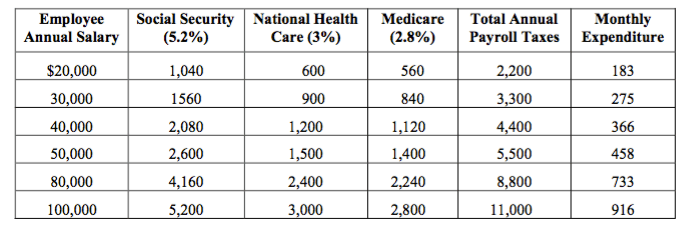

Because the tax on gross sales is so small, it allows for an expansion of payroll taxes to include an increase in the Medicare obligation, along with a new payroll tax for National Health Care. The proposed payroll taxes would look like this:

- The Medicare payroll tax will increase from 1.45% to 2.8%.

- The Social Security payroll tax will be reduced from 6.2% to 5.2%.

- The artificially imposed $110,100.00 cap on Social Security contributions has been removed. The employer must now continue to pay the lower 5.2% Social Security payroll tax no matter how high the annual gross wage might be.

- A 3% payroll tax for National Health Care has been added.

- Business payroll tax obligations now total 11% (compared to their current total of 7.65%

EXAMPLE – Examples of proposed Annual Payroll Taxes based on employee salaries:

Please note that health care expenditures make up 52.1% of total payroll obligations. When the savings produced from the Business Gross Sales Tax is added to the savings generated by funding National Health Care through payroll taxes, overall corporate tax liability declines.

c. Surplus Net Business Income (profit) Tax

All net income (profit) over $800,000 that has not been used after a period of two years is taxed at 50%. Since this money is prohibited from being used for company share repurchase, budgets for research and development, wages, and working conditions will increase making corporations stronger and more competitive.

d. Foreign Business Taxes

Section 1.d. addresses the problem of American workers losing their jobs to foreign workers due to the closing of manufacturing plants in the United States that are reopened in foreign countries. These factories are opened in countries that provide the cheapest labor, usually based on unfair wages and unsafe working conditions, and the least regulation regarding environmental protection. Section 1.d.iv addresses the problem by placing special taxes on products manufactured under these conditions. These special taxes will force foreign manufacturing costs to rise making them too expensive to export to the United States. This will encourage American manufacturers to keep their plants here, in the United States, and will save and create millions of American jobs.

2. IndividualTaxes

a. Payroll Taxes

Section 2.a. addresses the problem of individual tax deductions by eliminating the basis for their existence – personal income taxes. Eliminating personal income taxes removes the need for tax deductions and the tax attorneys and creative accountants currently used by high income earners to lower or avoid tax obligations.

Everyone’s income will now be taxed through payroll taxes, and payroll taxes will be based on annual gross income. Annual gross income will be redefined to include income earned from all sources, with no distinction made between labor and investments. By treating all income equally, everyone will be subject to the same rates of taxation.

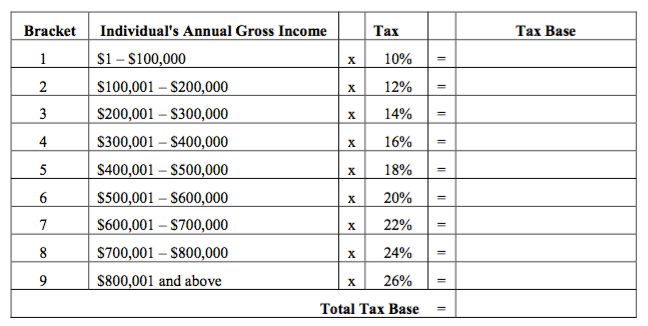

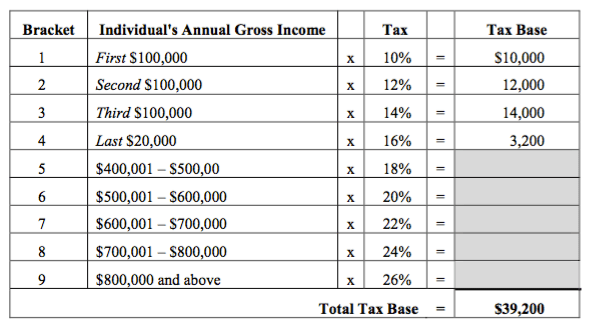

The annual gross income tax base upon which payroll taxes will be based will look like this:

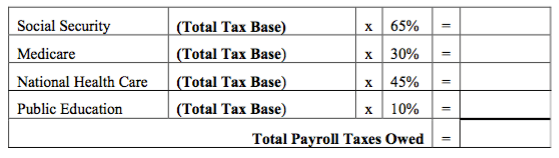

Payroll taxes will be applied against the Total Tax Base as follows:

EXAMPLE – To calculate the payroll taxes owed on annual gross income of $320,000:

- Separate the annual gross income into the appropriate bracket(s)

- Multiply by the corresponding tax, and place the results in the Tax Base column.

- Add up the results in the tax base column to determine the Total Tax Base.

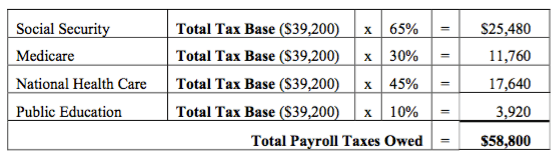

The Total Tax Base is then multiplied by the percentages associated with Social Security (65%), Medicare (30%), National Health Care (45%), and Public Education (10%), and added together to determine the Total Payroll Taxes Owed.

In this case, an individual with annual gross income of $320,000 would pay only $58,800 in payroll taxes, an effective tax rate of 18.38%.

Since the vast majority of Americans earn less than $100,000 annually, most taxpayers will fall into bracket #1, and will pay only 15% in annual payroll taxes. The increased payroll tax obligations will be accepted by a majority of taxpayers for three main reasons:

1. Overall taxes have been reduced.

2. People are no longer paying personal income taxes.

3. All citizens will be the beneficiaries of National Health Care, increased Social Security benefits upon retirement, and fully funded public schools that include free college or vocational school for all academically qualified students.

b. Tax Refunds

Partial refunds are sent to all eligible taxpayers whose earnings range from less than $11,000 annually for a single person, to a maximum of $25,000 for a four-person family.

3. Social Security, National Health Care, Public Education

a. Social Security

Social Security faces a future benefit pay out problem due to inadequate funding. If nothing is done to increase revenues, all eligible recipients will receive 100% of benefits through 2033, while after that benefits to recipients between the years 2034 and 2083 will be reduced by 23%.6

The solution to the future benefits pay out problem facing Social Security is accomplished by:

1. Removing the $110,100 cap on the business tax obligation to Social Security (1.b.)

2. Removing the $110,100 cap on the individual’s tax obligation to Social Security (2.a.)

3. Decreasing the business tax obligation to Social Security from 6.2% to 5.2% (1.b.)

4. Increasing the individual’s tax obligation to Social Security from 6.2% to 6.5%. (2.a.)

Section 2.a. eliminates the distinction between ordinary income and investment income and combines them into a common pool of money subject to the same rates of taxation. Because the caps on Social Security contributions have also been eliminated, only 11.7% of annual gross income (6.5% from individuals, and 5.2% from corporations) is needed to not only meet all future obligations, but to increase them as well. In fact, had this proposal been in effect in 2012, all 61.9 million recipients would have received an increase of $167/month.

b. National Health Care

National Health Care is simply an expanded version of Medicare. As a single-payer system, the government will replace private, for-profit health insurance companies to become the one and only health care administrator. As the sole administrator, the government becomes the collector of premiums in the form of payroll taxes, and the paymaster to the medical professions for the products and services they provide.

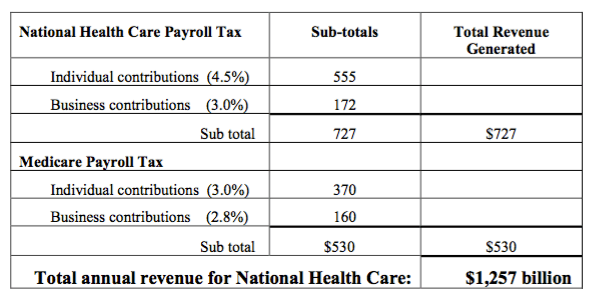

National Health will be financed by incorporating the funding from Medicare with the revenue raised by the new payroll tax for National Health, and from the general fund when necessary. The combination of Medicare and National Health Care payroll taxes (which amounts to 13.3% of annual gross income) will raise $1,257 billion per year as follows7:

In 2012, total US health care expenditures were $2,807 billion.8 Since this plan will reduce health care costs by a minimum of 40% ($1,122.8 billion), only $1,684.2 billion will be needed to fully fund National Health Care. However, because this plan only raises $1,257 billion from payroll taxes, we will be short $427.2 billion.

Fortuitously, this proposal creates a surplus of $179 billion when compared to the 2012 budget. Therefore, when we subtract the surplus from the $427.2 debt we find that only $248.2 billion from the general fund will be necessary to complete the full funding of National Health Care.

c. Public Education

Section 2.a.iv and Sections 8. fund public education at the federal level. This revenue, when combined with State and local revenue, is sufficient to create superior schools for all students in all neighborhoods. It equalizes funding for all schools from pre-school through grade 12, and allows all qualified students the opportunity to attend college or vocational school free of charge.

4. Value Added Tax (VAT)

Section 4 creates a 5% Value Added Tax (VAT) applied against all consumption except for spending on property (residential and commercial), speculative financial instruments (stocks, bonds, commodities, etc.), the sale of a business, gasoline, education, State and Local Government, Medicaid, Medicare, and National Health Care. It will raise $250 billion/year.

5. TransactionTaxes

Section 5 creates three new transaction taxes to increase revenues for the general fund:

a) 1% tax based on the purchase price of commercial and residential property, paid by the buyer at the time of the transaction;

b) 1% tax based on the purchase price of a business, paid by the buyer at the time of the transaction;

c) Wall Street Trading and Speculators Tax Act. U.S. Senate bill #1787 (112th Congress). This places a 0.03% transaction tax on the transfer of stocks, bonds, derivatives, and other debt securities.

6. EstateTaxes

Section 6. taxes the value of the deceased estate as follows: the first $3.5 million is exempt from taxation; above $3.5 million and up to $10 million the tax is 50%; above $10 million and up to $100 million the tax is 75%, and above $100 million the tax is 95%.

7. ExciseTaxes

a. Gasoline Tax

Section 7.a. increases the federal gasoline tax from $0.184 to $0.50 per gallon, and shall distribute the revenue as follows:

i $0.20 shall be allocated to the Highway Trust Fund for the repair, maintenance, and construction of our Interstate Highway system.

ii. $0.07 shall be allocated for the construction of mass transit projects.

iii. $0.03 shall be allocated to the Leaking Underground Storage Tank (LUST) Trust Fund

iv. $0.20 shall be allocated for construction of the infrastructure (grid) necessary for the nationwide implementation of renewable, nonpolluting energy sources and technologies.

In 2012, total US health care expenditures were $2,807 billion.8 Since this plan will reduce health care costs by a minimum of 40% ($1,122.8 billion), only $1,684.2 billion will be needed to fully fund National Health Care. However, because this plan only raises $1,257 billion from payroll taxes, we will be short $427.2 billion.

Fortuitously, this proposal creates a surplus of $179 billion when compared to the 2012 budget. Therefore, when we subtract the surplus from the $427.2 debt we find that only $248.2 billion from the general fund will be necessary to complete the full funding of National Health Care.

c. Public Education

Section 2.a.iv and Sections 8. fund public education at the federal level. This revenue, when combined with State and local revenue, is sufficient to create superior schools for all students in all neighborhoods. It equalizes funding for all schools from pre-school through grade 12, and allows all qualified students the opportunity to attend college or vocational school free of charge.

4. Value Added Tax (VAT)

Section 4 creates a 5% Value Added Tax (VAT) applied against all consumption except for spending on property (residential and commercial), speculative financial instruments (stocks, bonds, commodities, etc.), the sale of a business, gasoline, education, State and Local Government, Medicaid, Medicare, and National Health Care. It will raise $250 billion/year.

5. TransactionTaxes

Section 5 creates three new transaction taxes to increase revenues for the general fund:

a) 1% tax based on the purchase price of commercial and residential property, paid by the buyer at the time of the transaction;

b) 1% tax based on the purchase price of a business, paid by the buyer at the time of the transaction;

c) Wall Street Trading and Speculators Tax Act. U.S. Senate bill #1787 (112th Congress). This places a 0.03% transaction tax on the transfer of stocks, bonds, derivatives, and other debt securities.

6. EstateTaxes

Section 6. taxes the value of the deceased estate as follows: the first $3.5 million is exempt from taxation; above $3.5 million and up to $10 million the tax is 50%; above $10 million and up to $100 million the tax is 75%, and above $100 million the tax is 95%.

7. ExciseTaxes

a. Gasoline Tax

Section 7.a. increases the federal gasoline tax from $0.184 to $0.50 per gallon, and shall distribute the revenue as follows:

i $0.20 shall be allocated to the Highway Trust Fund for the repair, maintenance, and construction of our Interstate Highway system.

ii. $0.07 shall be allocated for the construction of mass transit projects.

iii. $0.03 shall be allocated to the Leaking Underground Storage Tank (LUST) Trust Fund.

iv. $0.20 shall be allocated for construction of the infrastructure (grid) necessary for the

nationwide implementation of renewable, nonpolluting energy sources and technologies.

b. National Resources Royalty Tax

Section 7.b. imposes for the first time a royalty of 12.5% on hard rock minerals, increases the royalty on coal from12.5% to 15% (based on gross value), and increases the royalty on gas and oil from 12.5% to a minimum of 18.5%, and under certain market conditions, to 25%.

8. State Reimbursement

Section 8. sends back to the States 30% of the non-income based tax revenue collected by the federal government, approximately $370.5 billion annually. This reimbursement money is allocated to each state based on each state’s population as a percentage of the total U.S. population, and directs how 100% of this money is to be spent.

Sub-sections 8.i, 8.ii, and 8.iii direct the States to fund research and development proposals for science, technology, and medicine; infrastructure projects; new public medical center teaching hospitals, and general acute care hospitals.

Sub-sections 8.i. – 8.o. direct the States to disperse their reimbursement money to their Counties, based on each County’s population as a percentage of the States population, to fund public education and other programs and services that benefit their residents.

Appendix F: Projected Tax Revenue

Appendix F presents the revenue generated from each of the taxes proposed in this plan, and this totals $3,716 billion. Of this $3,716 billion, $2,481 billion (67%), is raised through business and individual payroll taxes to specifically fund Social Security, National Health Care, and Public Education. The balance, $1,235 billion (33%), is generated from non-income based taxes and is used to fund all other government obligations.

In 2012 our government collected $2,450 billion,9 but spent $3,537 billion,10 creating a deficit of $1,087.0 billion.11 In contrast, had this proposal been in effect at that time, it would have produced a surplus of $179 billion.

1 http://act.credoaction.com/sign/sanderstaxloopholes?t=2&akid=13946.7934487.Juek6Y

2 http://www.ctj.org/corporatetaxdodgers/sorrystateofcorptaxes.php#The Size of the Corp

http://www.villagevoice.com/2012-10-10/news/the-10-most-corrupt-tax-loopholes/

http://www.washingtonpost.com/wp-dyn/content/article/2005/12/30/AR2005123001480.html https://sunlightfoundation.com/blog/2010/02/12/the-legacy-of-billy-tauzin-the-white-house-phrma-deal/ www.medicalsupplychain.com/pdf/Medicare%20Part%20D%20Reform%20&%20Coruption%20Issues.pdf http://sunlightfoundation.com/blog/2013/01/02/fiscal-cliff-lobbying/ http://www.americanprogress.org/issues/green/news/2012/02/07/11145/big-oils-banner-year

3 http://www.cbpp.org/cms/?fa=view&id=1258

4 https://www.whitehouse.gov/sites/default/files/omb/budget/fy2012/assets/receipts.pdf Table 15-5 Receipts by Source (Page 220)

5 See Appendix G

6http://www.ssa.gov/oact/tr/2013/tr2013.pdf

7 See Appendix F

8https://www.cms.gov/research-statistics-data-and-systems/statistics-trends-and- reports/nationalhealthexpenddata/downloads/proj2012.pdf See Table 1, page 5

9 http://www.usgovernmentrevenue.com/yearrev2012_0.html

10 http://www.usgovernmentspending.com/federal_budget_detail_2015bs22012n

11 http://www.usgovernmentrevenue.com/yearrev2012_0.html